If a company disposes of (sells) a long-term asset for an amount different from the amount in the company’s accounting records (the asset’s book value), an adjustment must be made to the amount of net income appearing as the first item on the SCF.

To illustrate, assume a company sells one of its delivery trucks for $3,000. The truck is in the accounting records at its original cost of $20,000. Its accumulated depreciation is $18,000. Combining the $20,000 and the $18,000 results in a book value (or carrying value) of $2,000.

Because the cash received/proceeds from the sale of the truck was $3,000 and the book value was $2,000 the difference of $1,000 is reported as a gain on the income statement. As a result, the company’s net income will increase by $1,000. (If the truck had sold for $1,500 there would be a $500 loss, which would reduce the company’s net income.)

One of the rules in preparing the SCF is that the entire proceeds received from the sale of a long-term asset must be reported in the section of the SCF entitled investing activities. This presents a problem because any gain or loss on the sale of an asset is included in the amount of net income shown in the SCF section operating activities. To overcome this problem, each gain is deducted from the net income and each loss is added to the net income in the operating activities section of the SCF.

We will demonstrate the loss on the disposal of an asset in Good Deal’s next transaction.

Please let us know how we can improve this explanation

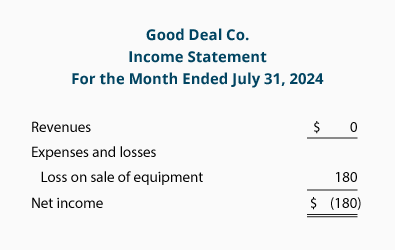

Submit Feedback No ThanksOn July 1, Matt decides that his company no longer needs its office equipment. Good Deal used the equipment for one month (June 1 through June 30) and had recorded one month’s depreciation of $20. This means the book value of the equipment is $1,080 (the original cost of $1,100 less the $20 of accumulated depreciation). On July 1, Good Deal sells the equipment for $900 in cash and reports the resulting $180 loss on sale of equipment on its income statement. There were no other transactions in July.

The income statement for the month of July will show how the disposal of the equipment is reported:

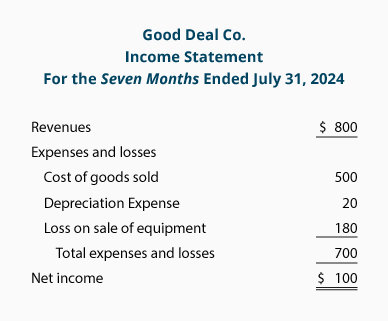

The income statement for the period of January 1 through July 31 is:

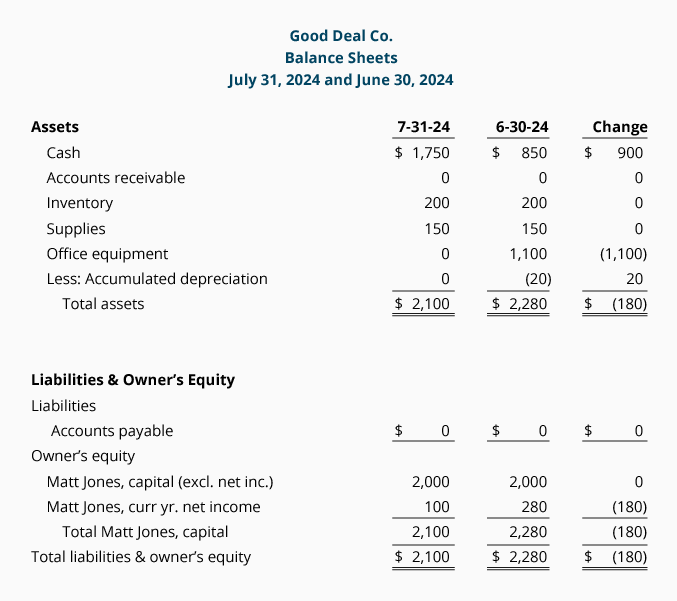

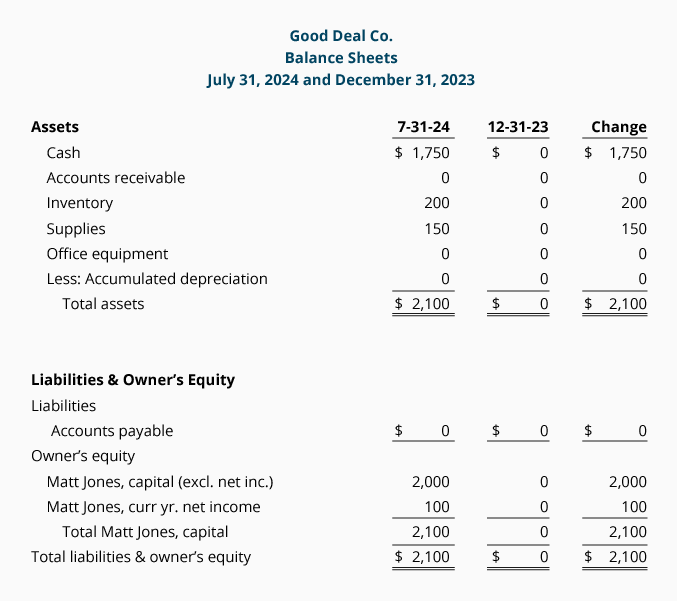

The following comparative balance sheet shows the changes that occurred during July:

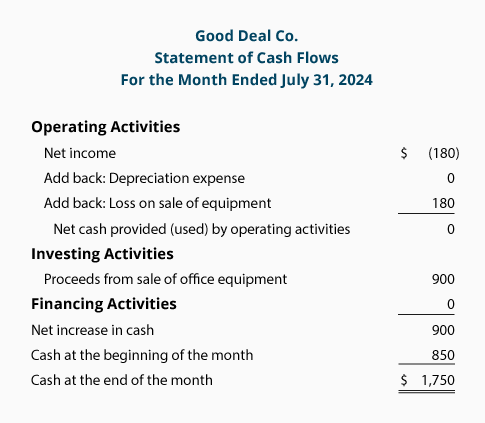

The SCF for the one month of July is:

Let’s review the cash flow statement for the month of July 2023:

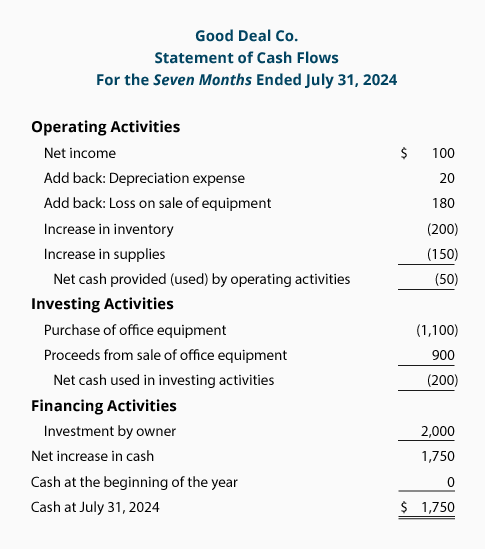

The SCF for the period of January 1 through July 31 is:

Let’s review the cash flow statement for the seven months of January through July 2023:

Net increase in cash during the seven months was a positive $1,750 (the combination of the totals of the three sections—operating, investing, and financing activities). This $1,750 agrees to the check figure—the increase in the cash from the beginning of January to July 31.

Please let us know how we can improve this explanation